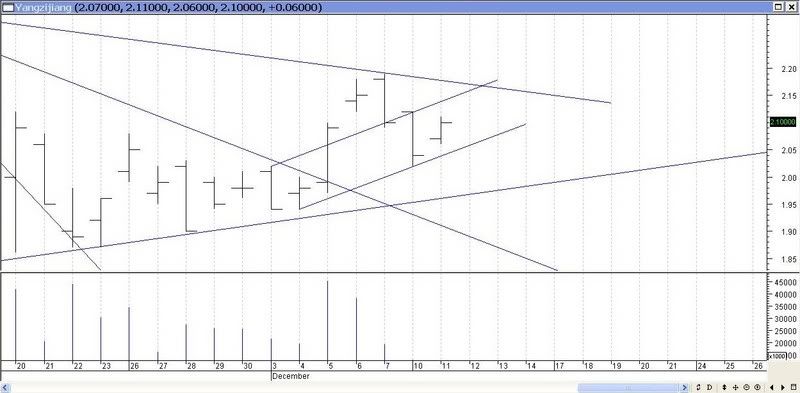

Although day low for Yangzijiang today is higher (@ 2.06 vs support @ 2.038), its high was also lower (@ 2.11 vs uptrend resistance @ 2.139).

Tomorrow's resistance is at about 2.15 to 2.17. If that breaks, we may see Yangzijiang testing 2.22 again.

Tomorrow's support is @ 2.058. If that breaks, may see it slip back to 1.98 or 1.96.

Good Luck !!

1 comment:

M O R G A N S T A N L E Y R E S E A R C H

December 12, 2007

Asia/Pacific Morning Meeting Summary

Rating: Overweight-V

China Shipbuilding: In-Line

Target: S$2.48

52-Week Range: S$0.56-0.24

Mkt. Cap(mn): Rmb27,143

ModelWare EPS: Rmb0.24 (FY 12/'07),

Rmb0.41 (FY 12/'08)

YAZG.SI, Yangzijiang Shipbuilding (Holdings) Ltd. (S$2.10) / Leading China’s

Push to Catch Up in Containerships

Morgan Stanley Asia Limited

Andy.Meng@morganstanley.com, Kate.Zhu, Karen.Zu

We initiate coverage of Yangzijiang Shipbuilding with an Overweight-V rating and S$2.48

price target. As a leading global player in medium-size containerships, YZJ should benefit from a secular growth opportunity as China seeks to catch up in this segment of the industry. We see the

company’s receipt of an order for 16 containerships as a positive catalyst and expect the stock to

re-rate in the next 3-6 months.

Leading player in medium-size containerships: Yangzijiang’s 28% global market share in the

2,500 TEU category and 19% in 4,250 TEU compares favorably with China’s lagging

performance in the containership segment, where it has only 19% global market share vs. 47% in

bulk carriers and 28% in tankers.

Breakthrough in domestic market: The order for 16 containerships from China Ocean

(COSCO) marks a breakthrough for YZJ. In the past, more than 90% of YZJ’s orders have come

from overseas, but we expect it to enjoy better growth opportunity in domestic market in light of

Chinese shipping companies’ recent large IPOs and forthcoming expansion.

Top pick despite concerns on US slowdown: YZJ is our top pick in Chinese shipbuilding, as it

offers significant growth potential, while its valuation is attractive. Given its cost-cutting

advantage, YZJ should outperform other Chinese listed shipyards through the industry cycle,

despite our medium-term bearish view that a US slowdown could weaken shipbuilding demand.

Risks to our price target: 1) Peaking of global shipbuilding cycle; 2) significant cost inflation that

erodes margins; 3) production bottlenecks that delay deliveries.

China Shipbuilding: Initiating Coverage: Global Leader, Made

Post a Comment